2026–27 Federal Budget: What It Means, What the Numbers Show, and What We Think

1. A Premature Analysis: Hope Is Useless

I'm writing this prematurely, I know. None of it has been legislated. Parliament still needs to pass these measures, the Senate crossbench will have its say, and there is every chance that what was announced emerges from the legislative process looking quite different. I genuinely hope that is the case.

But I think it's important that we turn our minds now to what the world of wealth management looks like in a potentially new tax environment – because if these measures do pass in their current form, the implications for how Australians structure, build and protect their wealth are significant. The worst thing we can do is wait.

So consider this a planning exercise. I am hoping it turns out to be a complete waste of time.

Now. About the government.

This Budget represents a profound structural shift in how private capital is taxed in Australia. It is ambitious, sweeping, and — in several key areas — economically consequential. Whether it ultimately proves constructive or damaging will depend on legislative detail and behavioural response. But there is no question: the framework for building and holding wealth has changed.

"It's a responsible Budget, and a reforming Budget, which builds resilience and bolsters our economy. There is more cost‑of‑living relief, more Medicare and more aged care, and more housing. It makes the tax system fairer and stronger for workers, businesses, first home buyers and future generations. This is the most important and ambitious Budget in decades."

Fairer and stronger for businesses? Come on. Fairer for future generations? The same tools that have allowed Australians to build wealth for decades are being taken away from the very next generation trying to get started. More housing? The Budget papers themselves – in Statement 4, buried where they hoped nobody would look – contain this remarkable admission:

"The key reason housing has become less affordable isthat housing supply has not kept pace with rising demand."

Supply. Not investors. Not negative gearing. Not capital gains tax. Supply. And yet the centrepiece of this Budget's housing reform is to attack the demand side – specifically, to make it less attractive for investors to hold residential property. They acknowledge the problem is supply. Then they announce measures that will, in the short term, reduce rental supply as investors exit before the July 2027 deadline. The government has read its own budget papers. It just chose to ignore them.

Let's get stuck into it.

2. What Has Actually Changed

This analysis is based on the measures as announced in the Budget papers on 12 May 2026. Final outcomes will depend on legislative drafting, transitional provisions and potential amendments during the parliamentary process. Certain structural details — particularly around cost base treatment and entity interaction — may evolve.

Let me be precise about what was announced, because the detail matters enormously. These are the primary changes, in my opinion, and they interact with each other in ways that are not immediately obvious.

Capital Gains Tax — The End of the 50% Discount

From 1 July 2027, the 50 per cent CGT discount that has been the foundation of long-term investment in Australia since 1999 will be replaced with:

Cost base indexation: Only the 'real' gain – the gain above inflation – is taxable. The cost base is adjusted for CPI each year.

A 30 per cent minimum tax rate: Applied to the real (inflation-adjusted) gain. If your marginal rate is above 30%, you pay the top-up. If below 30%, the 30% floor applies.

A surprise: pre-1985 CGT assets are brought in. Assets acquired before CGT began in 1985 – which many long-standing families have held for decades – are now brought into the regime for gains accruing from 1 July 2027. Gains before that date remain exempt.

Transitional arrangements: The 50% discount continues to apply to gains accrued before 1 July 2027. Assets held at that date are effectively split – the pre-2027 gain is taxed under old rules, the post-2027 gain under new rules.

New residential builds: exempt. Investors buying new builds can choose either the 50% discount or the new indexation regime – whichever is more favourable.

What this means in plain English: The CGT reform applies to everything: shares, businesses, investment properties, pre-1985 assets. The only carve-outs are superannuation (completely untouched – the 1/3 discount inside super continues unchanged) and new residential builds (investor choice). For everything else, the rules change fundamentally from 1 July 2027.

Negative Gearing — Existing Properties Locked Out

From 1 July 2027, negative gearing on residential property will only be available for new builds. Investors who buy existing residential properties can no longer deduct net rental losses against their other income.

Grandfathering: Properties you hold at Budget night (7:30pm AEST, 12 May 2026) are fully grandfathered. Nothing changes for your existing negatively geared investments.

The quarantine rule: Losses from established residential properties acquired after 1 July 2027 can only be offset against residential property rental income – not against wages, salary or other income. They carry forward but are quarantined.

Shares are unaffected: The negative gearing reform applies only to residential property. Interest on borrowings to invest in shares, businesses or other assets remains fully deductible. This is an important distinction.

New builds exempt: Investors in new residential properties retain full negative gearing deductibility. The logic is to redirect incentives toward new supply rather than competition for existing stock.

I understand the argument. I even have some sympathy for it. Negative gearing on existing properties does not add a single home to the housing stock. It redirects capital from productive uses to leveraged speculation on existing assets. The problem is what you do about it.

Discretionary Trusts — The 30% Minimum

From 1 July 2028, a 30 per cent minimum tax will be imposed on all income distributed from discretionary trusts. This is the change that will have the most direct impact on how affluent Australian families structure their affairs.

How it works: The trustee pays 30% upfront. Beneficiaries declare the income and receive a non-refundable credit. Non-refundable means: if your marginal rate is below 30%, the overpaid tax is not returned. The ATO keeps it.

Who is excluded: Fixed and unit trusts, superannuation funds, special disability trusts, deceased estates, charitable trusts. Primary production income and income for vulnerable minors also excluded.

Who is included — confirmed: The government has expressly confirmed that testamentary discretionary trusts (TDTs) fall within the regime. TDTs are not carved out, despite earlier speculation; income distributed from a TDT will be subject to the 30% minimum from 1 July 2028 on the same basis as any other discretionary trust.

The rollover relief window: Three years from 1 July 2027 to restructure from a discretionary trust into a company or fixed trust, with CGT and stamp duty relief. This is real and valuable.

The classic wealth management structure in Australia has been: discretionary family trust distributing to a bucket company, with another family trust as shareholder of that company. The trust distributed income flexibly to low-income family members (taxed at 0–19%), retained the balance in the bucket company (taxed at 30%), and the CGT discount flowed through on asset sales.

Under the new rules, the 30% minimum at trust level eliminates the income-splitting advantage almost entirely. Distributing to a student child on 19%? The trust pays 30% and the ATO keeps the difference. Distributing to the bucket company? The trust pays 30% and the company is assessed again on the full amount – 60 cents in the dollar. The structure that worked for a generation is now, in its traditional form, a tax trap.

We will come back to what the new optimal structure may look like. But first, let me address the single most important tax issue in this Budget that almost nobody is talking about.

The Quiet Attack on Business and Innovation

The negative gearing changes were well-telegraphed. The CGT changes were expected. What was not well understood – and what I think is the most damaging element of this Budget – is that the CGT reforms apply not just to property. They apply to everything.

Shares. Business interests. Start-ups. The person who spent fifteen years building a business from nothing, skipped salary in the early years, took on all the risk, created jobs, and finally sold it – they face the same new CGT framework as a speculative property investor. That is not a coincidence. It is a policy choice. And it is the wrong one.

I return to this point twice later in the paper: in the worked example, where a high-growth business founder pays roughly $1,737,912 more in tax under the new rules, and in the policy recommendations, where I propose separating business CGT from property CGT and introducing a tax-free threshold on founder exits.

3. The Other Announcements

In fairness, the Budget contained measures worth acknowledging. They do not offset the structural damage of the CGT and trust changes, but they deserve an honest mention.

Tax Cuts for Workers

A new Working Australians Tax Offset (WATO) of $250 per year from 2027–28, plus a $1,000 instant work-related expense deduction from this year's return. Combined with previous rounds of tax cuts, the Government estimates average earners will be up to $2,816 better off per year from 2027–28 compared to 2023–24 settings.

Welcome. But let's be clear about what this doesn't fix: bracket creep. More on that shortly.

Business Measures

A few genuine positives here:

Permanent two-year loss carry-back for companies up to $1 billion turnover from 1 July 2026 – a real cash flow tool for businesses that hit a rough year.

Loss refundability for start-ups in their first two years from 1 July 2028 – genuinely useful for early-stage businesses burning cash.

Permanent $20,000 instant asset write-off for small businesses from 1 July 2026.

R&D Tax Incentive reforms from 1 July 2028 with higher offsets for genuine experimental activity.

These are good measures. They will help. But they sit alongside CGT changes that simultaneously make the reward for building a successful business significantly smaller. You cannot incentivise risk-taking with one hand while taxing the upside with the other and call it a pro-business budget.

Housing

Beyond the negative gearing and CGT changes: $47 billion total housing investment, $2 billion Local Infrastructure Fund targeting up to 65,000 new homes over the decade, expanded 5% deposit scheme for first home buyers, 80,000 new rental homes via build-to-rent strengthening, extended ban on foreign purchases of established dwellings until June 2029.

The Government's own dwelling investment forecasts tell the real story: 5% growth in 2025–26, slowing to 4% in 2026–27 and 3.5% in 2027–28. Supply is growing, but decelerating – and that's before the construction cost shock from the Middle East conflict fully flows through. PVC prices jumped 30% in April alone.

Superannuation

Nothing changes. The tax settings inside superannuation – 15% in accumulation, an effective 10% rate on gains held more than 12 months, zero in pension phase – are completely untouched. The superannuation performance test is being reformed to reduce barriers to investment in energy and housing, which is sensible.

This is the most important thing in the super section. Everything else changes. Super does not. I guess they probably feel like they've toyed with it for long enough. Anyway, we will return to this later, where super sits as the third gear of the post-Budget structure – the SMSF in pension phase, taxed at zero, on everything, forever.

A few important qualifications on super that are often misunderstood and matter for structuring decisions:

Transfer Balance Cap (TBC): Only $1.9 million can be transferred into pension phase (the tax-free environment). Any balance above the TBC must remain in accumulation and is taxed at 15% on earnings. So 'zero tax in pension phase' applies only up to $1.9 million in that phase – not to the entire super balance.

Division 293 (already in force): High earners with income plus concessional contributions above $250,000 already pay an additional 15% tax on concessional contributions, effectively doubling the contributions tax from 15% to 30%. This has been in force since 2012.

Division 296 (in force from 1 July 2025): An additional 15% tax applies on earnings – including unrealised gains – attributable to total super balances above $3 million. Critically, this applies to the total super balance across both accumulation and pension phase, not just accumulation. The tax is proportional – only the proportion of earnings attributable to the excess above $3 million is taxed. For example, with a TSB of $4 million, 25% of earnings ($1M/$4M) attract the additional 15%. The $3 million threshold is not indexed to inflation.

Non-concessional contributions: Clients with a total super balance at or above $1.9 million at 30 June cannot make non-concessional contributions at all. The bring-forward rule is also restricted for balances between $1.66 million and $1.9 million. This is a material constraint for high-balance clients.

Despite these qualifications, superannuation remains the most tax-effective wealth accumulation structure available to Australians. Even with Division 296, paying 30% on a proportion of earnings inside super is significantly better than 47% outside it. The strategy is not to cap super balances artificially, but to maximise contributions and manage the structure intelligently.

Cost of Living & Fuel

A $14.8 billion package responding to the Middle East oil shock: fuel excise halved, $10 billion Australian Fuel Security Reserve, gas exports reserved 20% for domestic users. These are genuine cost-of-living measures. They are also temporary responses to a temporary shock. They are not structural reform.

The Government had a structural option and walked past it. The 25 per cent LNG export tax — led by the Greens and Senator Pocock, with some analysts projecting it could raise around $17 billion a year, and polling strongly across the political spectrum — was ruled out by the Prime Minister before Budget night. Fifty-six per cent of Australian gas is exported with effectively no royalty take. The PRRT has under-collected for a decade. A serious cost-of-living response would have been to reform the resource rent take and use the receipts to fund permanent relief. Instead we got a cheque, a reserve, and a domestic reservation that does not start until 2027. The contrast with the trust and CGT measures is hard to miss: structural reform was available when it suited the Government's politics, and declined when it did not.

4. What the Numbers Actually Show

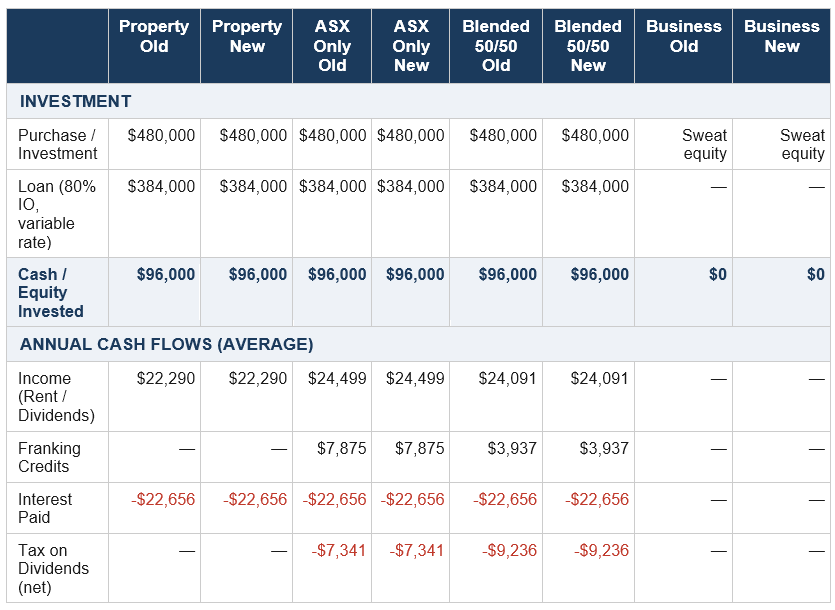

Theory is one thing. Let's look at what these changes actually mean in dollar terms. We have modelled four scenarios, all starting with the same $480,000 investment in January 2010, sold at end of 2024 – a Melbourne investment property, an ASX-only share portfolio, a blended 50/50 ASX and international (S&P 500 via IVV) portfolio, and a high-growth sweat equity business. We have run each under the current rules and the new rules, as if the new rules had always applied.

All figures calculated year by year using actual data – not averages. Interest rates use actual RBA F5 IO investor variable rates each year. Share portfolios use actual ASX 200 year-end index values and year-by-year dividend yields.

What the Table Tells Us

Property — Surprisingly Nuanced

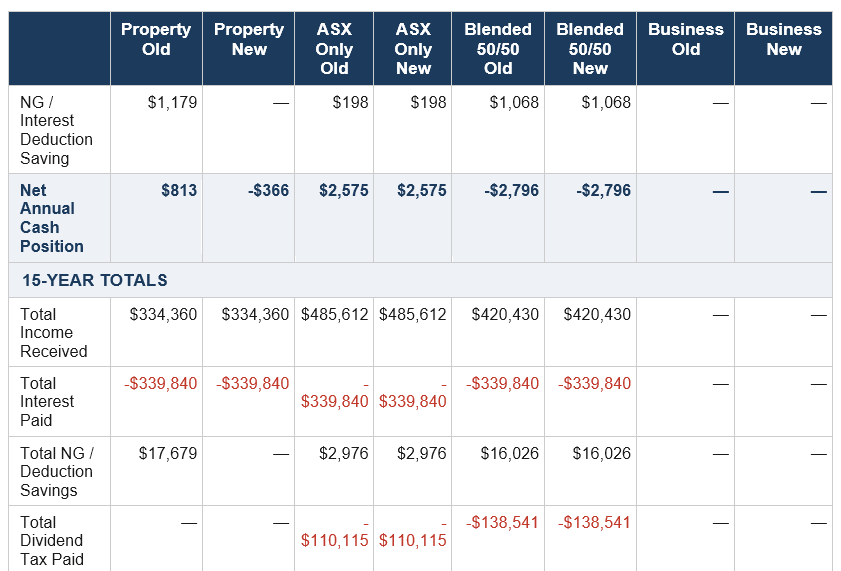

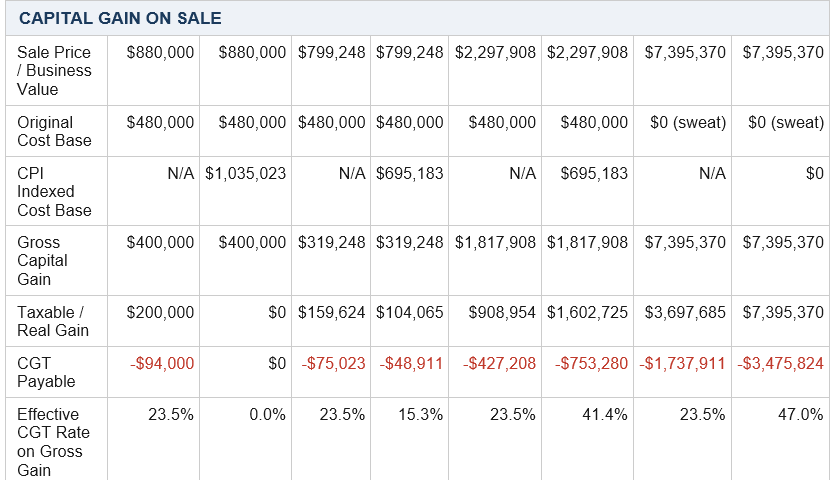

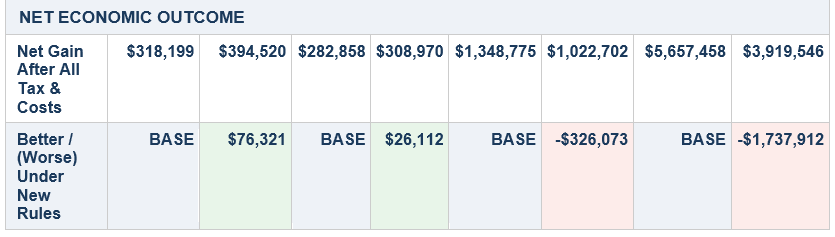

The property investor ends up $76,321 better off under the new rules. Zero CGT payable. Why? Two things work heavily in their favour: first, under the new rules all the denied interest deductions – $339,840 over 15 years – get added to the cost base. Second, CPI indexation then inflates that adjusted cost base further. Together, the total adjusted cost base reaches $1,035,023, exceeding the $880,000 sale price entirely. No real gain. No tax.

One important nuance: when we calculate the negative gearing savings year by year rather than using averages, the picture changes materially. In 2010 and 2011, IO variable rates were 7.4–7.55% against rent of only $330–350 per week. Annual losses of $10,000–$11,000, annual tax savings of around $4,700–$5,200. Properly calculated year by year, the total negative gearing tax saving under the old rules over 15 years was $17,679 – nearly seven times what a simple average would suggest.

It is also worth noting that interest capitalisation – adding interest to the cost base rather than deducting it annually – is a separate strategy that becomes relevant under the new rules for certain asset types. For non-income-producing assets like vacant land or properties under construction, capitalising interest is orthodox and well-supported, and can further compress the taxable gain on exit. We will be exploring this with clients on a case-by-case basis.

Note: our modelling assumes the entire adjusted cost base – purchase price plus capitalised interest – is indexed by CPI as a single figure. This is the most logical interpretation based on existing CGT framework mechanics, but is subject to confirmation once the exposure draft legislation is released.

The property numbers are less alarming than the headlines suggest. But that misses the point. The alarming part is what happens to investment behaviour before July 2027 – investors exiting existing properties, reducing rental supply, pushing up rents – before any new supply arrives to replace them.

Shares — It Depends on Where You Invest

The ASX-only portfolio is the one scenario where the investor ends up better off under the new rules – and it is worth understanding why. The portfolio grew from $480,000 to $799,248 over 15 years – capital growth that barely outpaced inflation. CPI indexation strips out most of the nominal gain, leaving a real gain of only $104,065. The investor pays 47% on that real gain, producing CGT of $48,911 – materially lower than the $75,023 under the old rules. And critically, interest deductibility on shares is completely unchanged. The result: $26,113 better off.

Now look at the blended portfolio, modelled year by year using actual IVV USD prices and AUD/USD exchange rates. The S&P 500 component delivered exceptional returns in USD terms, and the AUD's decline from above parity in 2010 to ~$0.62 by 2024 added a substantial FX tailwind. The blended portfolio grew to $2,297,908. Real growth well above inflation. The indexed cost base of $695,183 barely touches the $1,602,725 real gain. The investor pays 47% on that real gain – CGT of $753,281 versus $427,208 under the old rules. The investor is $326,072 worse off – entirely driven by the CGT increase on a genuinely high-growth portfolio.

These two columns sitting side by side make the most important point: the new rules are growth-rate sensitive. For the ASX-only portfolio, where capital growth barely beat inflation, the new rules actually produce a better outcome. For the blended portfolio with genuine international growth well above inflation, the new rules are materially worse. The more successful the investment, the harder the new rules hit. That is not an accident. It is the design. And it is the wrong design.

Business — Where It Gets Ugly

This is the number that matters. The sweat equity founder – zero cost base, built from nothing – pays $1,737,913 more in tax under the new rules. Under the old rules: $1,737,911 CGT at an effective 23.5% rate. Under the new rules: $3,475,824 at a full 47% marginal rate. Why 47% and not 30%? Because the 30% is a 'minimum' – it is a floor, not the rate. For a top-rate taxpayer, their 47% marginal rate applies to the real gain, and since 47% exceeds the 30% floor, they pay 47%. The entire $7,395,370 sale price is taxable – there is no cost base to index, no interest to add, no inflation to strip out. The new rules hit the full gain at the full marginal rate.

There is a particularly cruel irony here. The Government has framed the new CGT rules as fairer because they tax only 'real' gains – gains above inflation. CPI indexation, they say, protects investors from paying tax on illusory gains driven by rising prices. That protection is real for someone who invested capital. But for a sweat equity founder who invested nothing – who built something from zero – CPI indexation on a zero cost base produces exactly zero benefit. Index zero by any number and you still get zero. The inflation protection that makes the new rules palatable for asset holders is entirely, mathematically unavailable to the person who had no assets to begin with. The new rules are most punishing precisely for the people who took the greatest risk.

This is not about property speculation. This is about penalising success. The person who built something from nothing, who went without salary in the early years, who created jobs and economic value, walks away with $1,737,912 less under the new rules than they would have under the old. That is the budget's most damaging legacy.

One important caveat on the business scenario: the small business CGT concessions – the 15-year exemption, the 50% active asset reduction, the retirement exemption (up to $500,000 lifetime), and the rollover relief – may significantly reduce or eliminate CGT for qualifying businesses. To access these, the business generally needs turnover under $2 million or net assets under $6 million, and must satisfy the active asset test. Our scenario does not model these concessions, which means the actual CGT liability for a qualifying small business founder could be materially lower than shown.

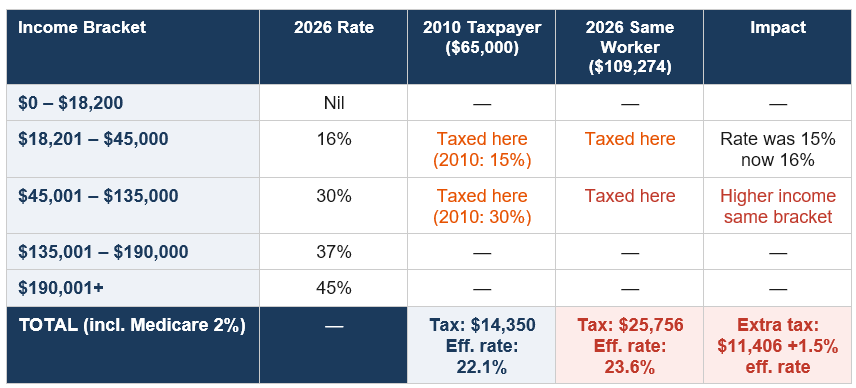

5. The Tax Nobody Talks About: Bracket Creep

While everyone focuses on the announced changes, the most insidious tax in Australia operates silently, every year, without a single vote in Parliament. Bracket creep – the phenomenon by which inflation and wage growth push ordinary workers into higher tax brackets – is a permanent, compounding tax increase that requires no legislation to implement.

Australia's personal income tax brackets are not indexed to inflation. They never have been. The Government periodically throws workers a bone – a modest tax cut here, an offset there – and calls it relief. But they never fully give back what inflation has silently taken.

The numbers: same worker, 16 years apart

For illustration, this example applies today's bracket structure to inflation-adjusted income to demonstrate the effect of bracket creep over time.

Consider a worker earning $65,000 in 2010. By 2026, with wages growing at roughly 3.3% per year – broadly consistent with average wage growth over the period – that same worker is now earning approximately $109,274. They have not had a real pay rise. They have had an inflation pay rise. Their purchasing power has barely moved. But their tax bill has grown significantly.

In 2010 they paid $14,350 in tax at an effective rate of 22.1%. By 2026 they pay $25,756 at 23.6%. That is $11,406 more in tax on exactly the same real income. The brackets have not moved. The worker has not been promoted. Inflation has simply done the Government's work for it.

The Stage 3 tax cuts helped. The new WATO helps at the margin. But none of it addresses the structural problem: a tax system that automatically becomes more punishing every year, silently, without debate or legislation.

Countries like the United States, Canada, and New Zealand index their tax brackets to inflation. Australia does not. This is a deliberate choice that generates billions in additional revenue for the Government every year without anyone having to vote for it. It is bracket creep. And it is a tax.

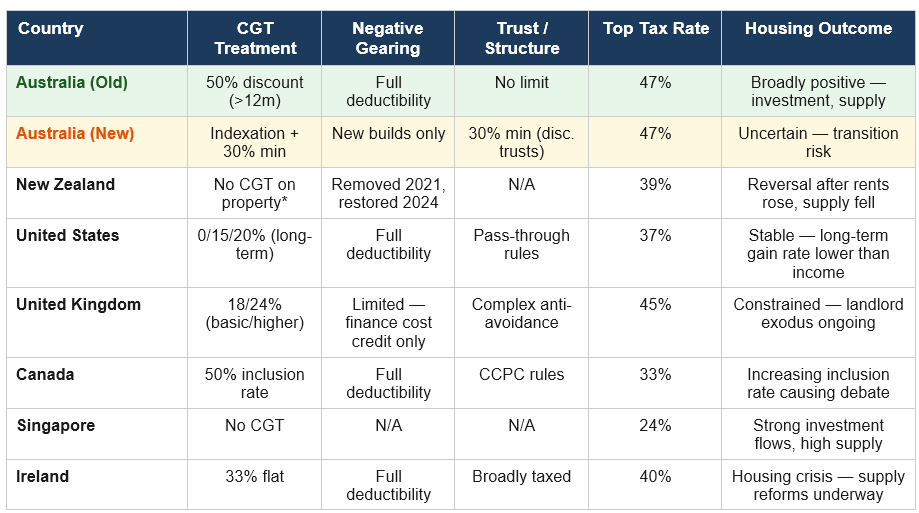

6. What Other Countries Are Actually Doing

Australia does not exist in a vacuum. Capital is mobile. Entrepreneurs make choices about where to build, invest and grow. It is worth examining how our peers approach these questions – not to simply copy anyone, but to understand what works, what doesn't, and what the evidence actually says.

The New Zealand Experiment: A Cautionary Tale

New Zealand tried this. It did not go well. And Australia, watching on, is implementing the same playbook.

October 2021: The Ardern Labour government removed interest deductibility on residential investment properties, phased over four years. The stated goal was to cool the housing market and improve affordability.

The period that followed saw rising rents and investor exit, alongside broader macroeconomic pressures including interest rate increases and post-COVID demand shifts. Attributing all rental market deterioration solely to the policy change would be too simplistic – but the direction of the effect was clear, and the policy did not achieve its affordability objectives.

October 2023: The National Party wins the election, campaigning partly on reversing the changes. The message from renters and property owners was unambiguous.

July 2024: Interest deductibility on investment properties fully restored. Three years. Gone. At significant economic and social cost.

The New Zealand experiment is not ancient history. It happened in our lifetime, in our timezone, in a country with almost identical housing market dynamics to Australia. The results were documented. The policy was reversed. And yet here we are.

The question that demands an answer: The New Zealand government tried this in 2021. It failed. They reversed it in 2024. Australia's government has watched this play out in real time, with real data, in a nearly identical market. Why are we implementing what has already failed?

What Other Countries Are Doing: The International Picture

A few things stand out from the international picture:

The United States taxes long-term capital gains at 0%, 15% or 20% – structurally lower than income tax rates. This is deliberate policy to incentivise long-term investment and entrepreneurship. You hold longer, you pay less.

Singapore has no capital gains tax at all. None. It has become one of the world's leading centres for wealth, investment, family offices and business. This is not a coincidence.

The United Kingdom has been restricting landlord tax benefits since 2015 – and is experiencing a sustained landlord exodus, rising rents and worsening rental affordability.

Ireland has a housing crisis despite (or perhaps because of) high capital gains tax and a complex property investment regime. Supply constraints, not investor behaviour, drive their crisis.

Canada recently increased its CGT inclusion rate and is facing significant debate about the impact on business investment, entrepreneurship and capital flight.

The pattern is consistent across jurisdictions: countries that tax capital gains lightly and provide clear incentives for long-term investment and entrepreneurship attract more of both. Countries that treat capital gains as equivalent to income see investment flows redirect toward lower-tax environments.

7. The Housing Supply Problem the Government Admitted But Ignored

Let me come back to that admission from Statement 4, because it deserves more than a passing reference.

"The key reason housing has become less affordable is that housing supply has not kept pace with rising demand."

— Treasury, Budget Paper No. 1, Statement 4, 2026–27

This is Treasury's own analysis. Supply. The problem is supply. And yet the centrepiece housing reforms in this Budget are: restricting negative gearing on existing properties – which affects demand, not supply; reforming CGT – which affects investor return calculations, not supply; extending the ban on foreign buyers – which affects demand, not supply.

The supply measures – the Local Infrastructure Fund, the build-to-rent reforms, the planning reform conditions – are genuine and worth having. But they are secondary in the Budget's narrative and secondary in their likely impact compared to the demand-side tax changes.

Here is the timeline problem. The tax changes take effect from July 2027. Investors holding existing properties will reassess. Some will sell. Rental supply will contract. Rents will rise. The new supply measures take years to produce actual dwellings. The gap between supply contraction and new supply arrival is where renters suffer.

We have seen this movie. It was filmed in Auckland between 2021 and 2024.

8. Wealth Structuring: The Old World and the New

For those of you who have built wealth through structures – family trusts, bucket companies, investment portfolios, business interests – this Budget changes the calculus significantly. Let me walk through what the old world looked like, why it worked, and what the new world looks like.

The Old Architecture: How It Worked

The classic Australian wealth structure had three interlocking parts working together:

Discretionary family trust: Held the family's investments and business interests. Distributed income flexibly each year to family members based on their tax position – children, spouse, retired parents. Effective rates could be as low as 0–19% on income that would otherwise attract 47%.

Bucket company: Excess income not needed by low-rate beneficiaries was distributed to a private company (the 'bucket') at 30% company tax. Profits accumulated there, compounding at a lower rate. Div 7A loans gave the family access to those funds.

Second family trust as shareholder: A second discretionary trust as shareholder of the bucket company added another layer of distribution flexibility – allowing the bucket company's dividends to be split again across the family on the most tax-effective basis.

CGT on exit: When assets in the trust were sold, the 50% CGT discount flowed through to beneficiaries. Distributed to a low-income family member, the effective CGT rate could be as low as 9.5% on a $1 million gain.

Why the New Rules Break This

The 30% minimum tax on discretionary trust distributions attacks the structure at its foundation. The income-splitting advantage – the entire reason the discretionary trust existed as a tax planning tool – is eliminated.

Here are the mechanics of why. When a trust distributes to a low-income beneficiary, the trustee now pays 30% minimum tax. The beneficiary receives a credit – but it is non-refundable. If the beneficiary's marginal rate is 19%, they pay 19% but the trustee has already paid 30%. The 11% difference is not refunded. The Government keeps it. Previously taxed at 19%. Now taxed at 30% with no refund. The arbitrage is gone.

The bucket company as a direct beneficiary of a discretionary trust is now effectively unworkable. A critical point has emerged from industry analysis of the Government's Fact Sheet: the trustee's 30% minimum tax does not reduce the income that flows through to the corporate beneficiary for assessment. Some practitioners initially assumed that the company would only be assessed on $70 out of every $100 distributed – as though the trust's 30% payment reduced the assessable amount. The Fact Sheet does not support that reading. The corporate beneficiary is assessed on the full $100, without any credit for the trustee's 30% tax. The result: the trust pays 30% and the company pays 30% on the same $100. Total tax: 60 cents in the dollar. That is not a structure. That is a tax trap.

The second family trust as shareholder of the bucket company is equally problematic. Any distributions from that second trust will attract the 30% minimum at trust level, and the bucket company is then assessed again on the full amount. Both layers appear unworkable under the new rules and will need to be reconsidered.

The New Architecture: Where to Go From Here

Before anything else, the right question to ask is not 'what structure should I have' but 'what do I need my structure to do?' The answer to that question determines everything else. If you need succession and intergenerational transfer – the discretionary trust still does that better than anything else. If you need tax-efficient investment accumulation – the unit trust with a bucket company as unitholder is worth exploring. If you need long-term compounding with maximum tax efficiency – superannuation, nothing changes there and nothing comes close. If you need asset protection and family law insulation – the discretionary trust again; a unit trust with fixed entitlements is more exposed. If you need all of the above – you may need more than one structure, each doing what it does best. The structure follows the objective. That has always been true. The new rules simply make it more important to be deliberate about which objective each structure is serving.

The good news is that the architecture does not need to be abandoned. It needs to be repositioned. And there is a three-year rollover relief window from 1 July 2027 to restructure with CGT and stamp duty relief. The window is real. It is generous. Do not waste it.

But here is the critical reframing: the discretionary trust does not get replaced. It gets repositioned. Under the old rules, the discretionary trust wore two hats simultaneously – it was the tax planning vehicle and the succession vehicle. The new rules strip away the tax hat. The succession hat remains very much intact. The question is no longer 'should I have a discretionary trust' but rather 'what should sit inside it, and what should sit alongside it'.

The Discretionary Trust — Repositioned, Not Replaced

The discretionary trust remains the right vehicle for succession and intergenerational wealth transfer, asset protection, family law protection, business continuity, and primary production. The trustee's discretion to distribute to beneficiaries across generations – children, grandchildren, future family members – without triggering CGT or stamp duty on the underlying assets is a powerful and irreplaceable tool. A fixed trust cannot do this.

The tax cost of the discretionary trust under the new rules is the 30% minimum on distributions. For clients where the succession, asset protection and family law benefits justify that cost – and for many they will – the discretionary trust remains entirely appropriate.

The Unit Trust — The Tax-Efficient Investment Vehicle

Where the priority is tax efficiency on investment income and capital gains – rather than succession flexibility – the unit trust is the right vehicle. Fixed entitlements mean it is excluded from the 30% minimum tax entirely. CGT and income flow through to unitholders at their own rate, once, without the pre-paid non-refundable minimum sitting underneath.

The unit trust is well-suited for investment portfolios, new build property, and joint ventures where multiple parties have agreed, defined stakes. The trade-off: the unit trust gives you tax efficiency but surrenders succession flexibility. You cannot change who holds what without a formal transfer of units.

The Optimal Structure — Both, Purposefully

For most sophisticated family structures, the answer is not one or the other. It is both, each doing what it does best:

Discretionary trust: Holds long-term family assets where succession, protection and intergenerational flexibility matter most. Accepts the 30% minimum as the cost of its structural utility.

Unit trust: Holds investment assets where income and CGT flow-through efficiency is the priority. Excluded from the 30% minimum. Corporate trustee provides governance and liability protection.

Bucket company — via fixed trust: The bucket company remains viable but only as a unitholder in a unit trust – not as a beneficiary of a discretionary trust. Because unit trusts are excluded from the 30% minimum, income flows to the bucket company at the unit trust level without the trust-level tax applying first. The company is assessed once at 30%. Clean and workable. By contrast, distributing from a discretionary trust to a bucket company now results in the trust paying 30% and the company being assessed again on the full amount – effective rate of 60 cents in the dollar. This is an area where careful structuring advice will be essential.

Reconsidering the discretionary trust layers above the bucket company: Both the primary discretionary trust distributing to the bucket company and the second family trust as shareholder of the bucket company appear problematic under the new rules. The second trust attracts the 30% minimum on distribution, and the company gets no credit. Direct individual or SMSF shareholding in the bucket company may be worth exploring.

Superannuation as the primary long-term accumulation vehicle: Nothing in this Budget touches the core super tax settings. In accumulation: 15% on earnings, effective 10% CGT on long-term gains. In pension phase: 0% on earnings up to the Transfer Balance Cap ($1.9M). Div 296 applies proportionally above $3M TSB across both phases. Div 293 applies 30% contributions tax for high earners above $250k. Non-concessional contributions nil if TSB ≥ $1.9M. Despite these qualifications, super remains the most tax-effective structure available to Australians.

The key insight: the discretionary trust is no longer the tax vehicle. It is the succession vehicle. These are not the same thing.

The Company as a Negative Gearing Vehicle

One structural opportunity that the new rules inadvertently create: based on the announcement, the restriction appears targeted at individuals and trusts holding residential property. A company borrowing to acquire investment assets – including potentially existing residential property – may still be able to deduct interest in the ordinary way. This is subject to legislative confirmation, but if correct it creates an interesting planning opportunity.

Losses accumulate in the company, carry forward indefinitely (subject to continuity of ownership), and can ultimately be offset against the capital gain on sale.

Alternatively, for non-income-producing assets – development sites, vacant land, properties under construction – capitalising the interest to cost base rather than deducting it annually produces a higher cost base on exit and a lower taxable gain. This is orthodox, well-supported by existing tax principles, and becomes more relevant under the new rules.

The caveat, and it is an important one: getting money out of a company is taxed. Franked dividends at 47% less the 30% franking credit equals 17% top-up. Total effective rate approximates the marginal rate. The company is a deferral vehicle, not a permanent shelter. The SMSF is the permanent shelter.

9. Our View: What This Budget Gets Wrong, and What Good Policy Looks Like

I want to be direct. I have tried to be balanced in this analysis – acknowledging what is reasonable in the Government's position, being honest about where the numbers are more nuanced than the headlines suggest. But there are things in this Budget that I think are genuinely wrong, and I am not going to pretend otherwise.

What the Budget Gets Wrong

1. The CGT framework applies too broadly. Limiting negative gearing to new residential builds – I can follow the logic. But applying the same CGT framework to shares, to businesses, to innovation, to the assets that actually create something? That is where the logic collapses. A property investor who buys an existing house and waits for capital growth creates nothing. An entrepreneur who builds a business creates jobs, products, services, economic activity.

2. The trust changes are a blunt instrument. Some discretionary trusts are used aggressively to minimise tax. Some are used for entirely legitimate succession planning, asset protection and family business management. A blunt 30% minimum tax does not distinguish between the two.

3. The housing analysis diagnoses the disease correctly and prescribes the wrong medicine. Treasury said it. Supply. The Government responded with demand-side measures. The New Zealand experiment showed exactly what happens. Rents rise. Supply contracts. The policy is reversed.

4. Bracket creep is a silent ongoing tax increase that this Budget does not fix. The $250 WATO and the $1,000 instant deduction are welcome. They are also entirely inadequate. Australia's tax brackets are not indexed to inflation. Every year, without legislation, the Government collects more tax from workers whose real income has not changed.

What Good Policy Would Look Like

On business and innovation CGT: a tax-free threshold for founders

The single most powerful thing this government could do to incentivise entrepreneurship is to separate business CGT from property CGT entirely. Apply the new rules to property – fine. But for gains from the sale of a business you built, a different framework applies.

The idea is simple: the first $5 million – or even $10 million – of gain on the sale of a business that has been operating for more than, say, five years is tax-free. The founder who spent years building something, took the risk, created jobs, and succeeded gets to keep the first $5 million without penalty.

With a $10 million tax-free threshold: the founder keeps $7,395,370 of their $7,395,370 gain. Zero tax. The entire reward for fifteen years of building flows to the person who created it.

With a $5 million threshold: the tax bill drops from $3,475,824 to $1,125,824 – a saving of $2,350,000. Still meaningful. Still a significant incentive to build.

Is this expensive for the Budget? Relatively. But consider what it buys: a generation of Australians willing to back themselves, start businesses, create jobs, take risks.

On housing: fix supply, not demand

The right housing policy is not about reducing the tax attractiveness of investment property. It is about building more homes. Faster approvals. More land. Better infrastructure. Genuine planning reform. The UK, Ireland and New Zealand have all restricted investor incentives in property. All have worsening rental affordability. Singapore, which taxes capital lightly and focuses on supply, has among the highest homeownership rates in the world.

On bracket creep: index the brackets

Every developed economy that takes fiscal fairness seriously indexes its tax brackets to inflation. It is not complicated. When wages rise with inflation, tax thresholds rise with inflation. Workers keep the same real share of their income. Index the brackets. It is the simplest, most honest structural reform available.

On trusts: target the abuse, not the structure

A minimum tax that targets specific aggressive trust arrangements – defined by distribution patterns, income types, beneficiary relationships – would be more defensible than a blanket 30% minimum. It would be harder to draft. It would require more nuance. But it would be fairer. And it would not catch the family business owner who has used a trust for thirty years as part of sensible estate planning in the same net as the aggressive tax minimiser.

10. The Bottom Line

This Budget, whether intentionally or not, makes it harder to build wealth in Australia. It makes it more expensive to succeed. It removes incentives that have underpinned investment, entrepreneurship and long-term wealth creation for a generation. And it does so while the Government's own papers acknowledge that the core problem it is trying to solve – housing affordability – is fundamentally a supply problem that these measures do not fix.

The New Zealand experiment was not a theoretical exercise. It was a real policy, implemented in a real market, that produced real harm to real renters over three years before it was reversed. Australia is following the same script. That is not speculation. It is pattern recognition.

The same tools that allowed the previous generation of Australians to build wealth – property investment, business ownership, trust structures, long-term share holdings – are the tools being made less available to the next generation. If you genuinely want young Australians to have a go, you give them the same tools, not fewer of them.

On the specific question of business and entrepreneurship: someone who spends years building a business, foregoes salary, takes on all the risk, creates jobs and economic activity, and eventually succeeds – that person should be celebrated and rewarded, not handed an extra tax bill of $1,737,912 simply because the Government changed the rules after they started. If this government genuinely wants to promote innovation and entrepreneurship, it should put a number to it. A tax-free threshold for founder exits. A real incentive to have a go.

Until then, good advisers will find the best path forward within whatever rules apply. The unit trust. The SMSF. The company as accumulation vehicle. The rollover relief window. There are always strategies. But strategies built around avoiding damage are not the same thing as strategies built around creating opportunity.

As always, good advice matters.

Ready to grow your wealth?

Let's talk. One call. No risk. Just a way to see if we're a good fit.