The SpaceX IPO. Let's be honest.

SpaceX went public. It did well. Nobody lost money on day one.

But I keep coming back to the weeks before it listed. The noise was something else. Jamie Dimon on a live simulcast to 2,500 clients across 26 states. Morgan Stanley projecting $3.4 trillion in revenue by 2040. Fidelity dropping its IPO minimum from $500,000 to $2,000. CNBC running a SpaceX segment every hour.

And here's the thing nobody seemed to want to say out loud. The same brokers telling you the stock is going up are the ones selling you the stock. Morgan Stanley didn't share that $3.4 trillion projection out of generosity. They had shares to move. Work it out.

When everyone is certain something can't go wrong, that's exactly when I get uncomfortable.

Not because SpaceX isn't a remarkable business. It is. Rockets, Starlink, defence, AI, infrastructure. Arguably one of the most consequential companies ever built. But here's a distinction worth keeping front of mind. Remarkable businesses and remarkable investments are not the same thing.

History is unambiguous on this point.

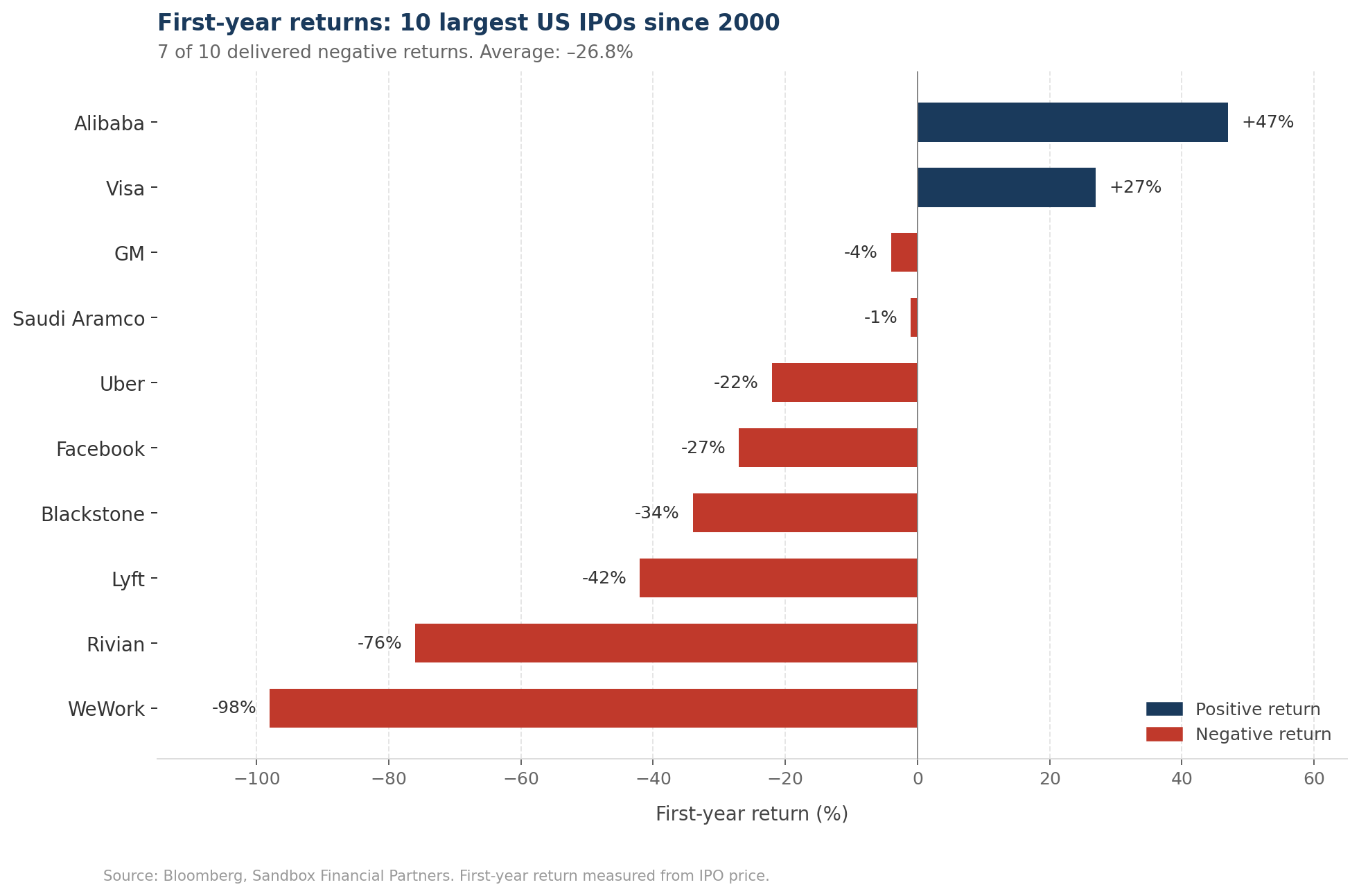

Of the 10 largest US IPOs since 2000, seven delivered negative returns in the first 12 months. The average? Down 26.8%. Meta. Blackstone. Uber. All great businesses. All poor early investments. Not because the companies were wrong. Because the price was wrong.

As Yale's Roger Ibbotson observed, investor enthusiasm creates a "superstar premium". You don't lose money by identifying the wrong company. You lose money by paying the wrong price for the right company.

We've been here before.

June 1966. A company called COMSAT went public. Space-age technology. Government backing. Massively oversubscribed. Investors lined up to buy shares "for their grandchildren". Within weeks, companies were adding "Astro" and "Orbital" and "Space" to their names just to ride the wave. The market topped that same year. The bear market that followed lasted 16 years.

I'm not saying SpaceX is COMSAT. I'm not saying short the stock.

What I am saying is that forecasting $3.4 trillion in revenue 14 years from now isn't analysis. It's salesmanship. Nobody in 2012 saw the pandemic coming. Or 500 basis points of rate hikes. Or two Trump elections. The world compounds in ways no model captures. The further out you look, the more ways things can go sideways.

The more useful question isn't what SpaceX is worth. It's where does the money come from. Every dollar flowing into this IPO has to come from somewhere. Index funds rebalance. Active managers feel pressure to own it. Retail investors sell existing positions to make room. That's where the volatility comes from.

SpaceX may be the most important company of our generation.

It may also be the beginning of the end of this particular cycle.

Both things can be true.

Process over prediction. Always.

Take the long view.

Ready to grow your wealth?

Let's talk. One call. No risk. Just a way to see if we're a good fit.